Israel’s technology sector has spent the last two years absorbing shocks that would flatten many national markets: prolonged security uncertainty, a stop-start global funding cycle, and a wave of consolidation among institutional investors. And yet capital keeps finding its way into the country’s startups. Making sense of israeli venture capital activity right now means separating headline totals from the more revealing story underneath: where the money is concentrated, which stages are actually getting funded, and why.

How much capital is actually moving through the market?

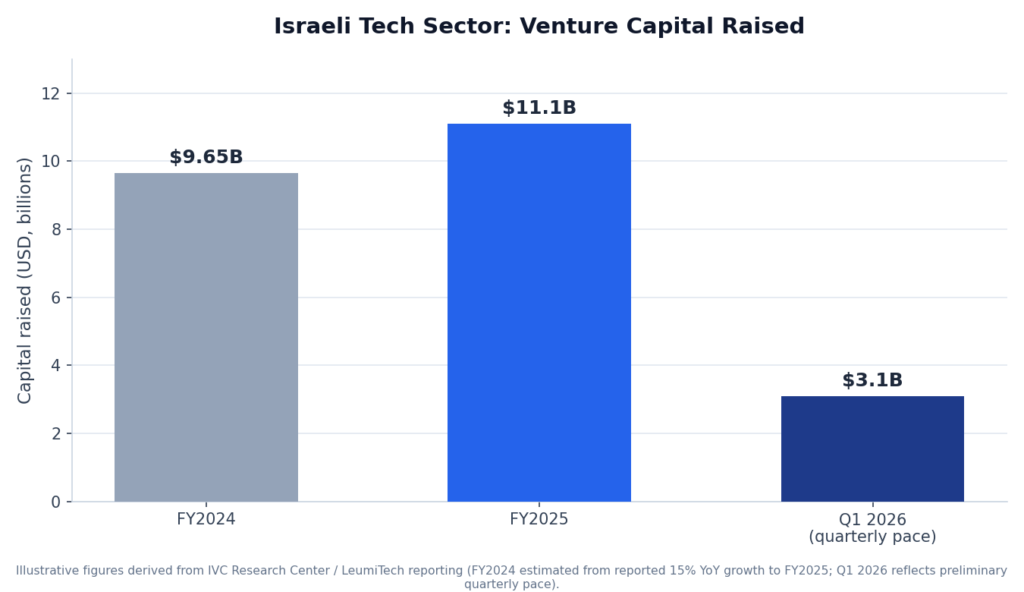

According to IVC Research Center and LeumiTech reporting, Israeli tech companies raised roughly $11.1 billion in 2025, an increase of about 15% over the prior year, even as the number of disclosed funding rounds declined. That combination, more dollars chasing fewer deals, is not a coincidence; it is the clearest fingerprint of a “flight to quality” that has defined the market since 2024. Preliminary 2026 figures point in the same direction: reporting citing IVC and LeumiTech data put first-quarter fundraising at roughly $3.1 billion, a 34% year-over-year increase, even though deal volume held flat at around 98 rounds.

Israeli tech venture capital raised, FY2024 vs FY2025 vs Q1 2026 quarterly pace. Figures derived from IVC Research Center / LeumiTech reporting; FY2024 is estimated from the reported 15% year-over-year growth to FY2025.

Why does capital concentrate so heavily at the top?

The same reporting found that the top decile of funding rounds accounted for roughly half of all capital raised in the first quarter of 2026, while foreign investors continued to supply close to two-thirds of the total. That concentration reflects how selective the market has become. Investors are not pulling back from Israel; they are narrowing their focus to founders and sectors with the clearest path to a return, which is exactly the environment in which experienced israeli vc firms, with long track records, existing portfolio relationships, and follow-on capital reserved for winners, tend to have an advantage over newer entrants.

What is pulling the largest share of that capital?

Cybersecurity remains the dominant vertical, by some measures accounting for roughly 40% of all capital raised in early 2026 reporting periods, a share reinforced by a run of large individual deals. Generative AI investment continues to run at a fairly steady share of total flow, while sectors more exposed to geopolitical risk, defense tech among them, have seen their relative share of quarterly funding shrink even as absolute activity in cybersecurity and AI has held up.

What changed at the early stage?

One of the more encouraging data points in recent reporting is the early-stage recovery. Pre-seed through Series A investment reportedly grew substantially since late 2023 and now accounts for a meaningfully larger share of total capital than in prior years, even as mid-stage Series B and C rounds have contracted as a share of the total. That divergence matters for the broader ecosystem: a healthy pipeline of new companies depends on early-stage capital being available, not just capital concentrated in follow-on rounds for already-proven winners.

This is also where the depth of the local venture capital bench starts to matter. Firms that have been through multiple market cycles, and that combine direct investment capital with hands-on company-building experience, tend to be the ones still writing early checks when newer or more opportunistic capital pulls back.

What should founders and investors take from this?

None of this means the Israeli market has become uniformly harder to raise in; it has become more selective. For a founder or an LP trying to read the market, the useful signal is not the headline total but the shape of where that capital is actually going.

- Expect diligence to take longer and bars to be higher, even for strong companies, in a “flight to quality” market.

- Sector matters more than it did two years ago; cybersecurity and applied AI are pulling a disproportionate share of available capital.

- Early-stage funding has genuinely reopened, but founders should expect investors to weight team and traction more heavily than in the 2021 environment.

- Relationships with established, multi-cycle investors carry more weight when capital is concentrated among fewer, larger rounds.

Frequently Asked Questions

Is Israeli venture capital funding growing or shrinking in 2026?

Based on IVC/LeumiTech data, total capital raised has been growing (2025 was up roughly 15% over 2024, and preliminary Q1 2026 figures were up 34% year over year), even though the number of individual funding rounds has stayed roughly flat.

Which sectors attract the most Israeli venture capital right now?

Cybersecurity has consistently been the leading vertical, accounting for a large share of total capital raised in recent reporting periods, with generative AI as the second most consistently funded category.

Is early-stage funding actually available again?

Reporting indicates pre-seed through Series A investment has grown substantially since late 2023 and now represents a meaningfully larger share of total capital than it did a few years earlier, even as later-stage rounds have contracted as a share of the total.